Most people assume that because they’ve been paying life insurance premiums for years, they can cash out whenever they choose. For term life insurance policyholders, that assumption leads to real confusion. Can you cash out term life insurance? The short answer is: not directly. Term life insurance is built around one purpose — paying a death benefit — and that design has significant consequences for anyone looking to access money from their policy. This guide breaks down why, explains what your real options are, and outlines the tax consequences you need to understand before making any decisions.

Table of Contents

Key takeaways

| Point | Details |

|---|---|

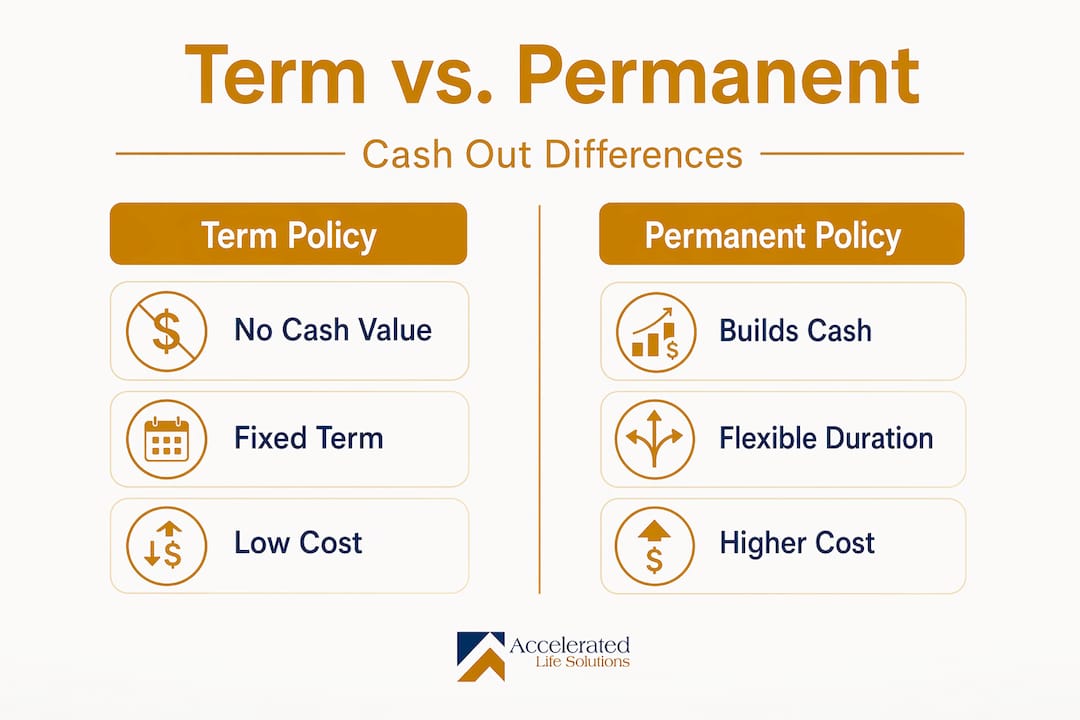

| Term policies have no cash value | Term life insurance is designed for death benefit only and does not accumulate cash you can withdraw. |

| Conversion is a viable path | A conversion rider lets you switch to permanent life insurance without new medical underwriting, unlocking future cash value growth. |

| Life settlements are an option | You may be able to sell your term life insurance policy to a third party for a lump sum under specific eligibility conditions. |

| Tax consequences are real | Surrendering or selling a policy above your cost basis triggers ordinary income tax on gains, ranging from 10% to 37%. |

| Act before conversion deadlines | Missing a conversion deadline by even one day eliminates your guaranteed right to convert, requiring full medical underwriting. |

Why you generally can’t cash out term life insurance

The confusion around cashing out term life insurance starts with how these policies are designed. Term policies last 10 to 40 years and exist solely to provide a death benefit for a defined period. When the term ends and no claim is made, the policy simply expires. No cash value builds. No refund is issued. You are paying for coverage, not an investment account.

This stands in direct contrast to permanent life insurance. Policies like whole life and universal life build a cash reserve over time that policyholders can access through loans, withdrawals, or full surrender. Term insurance was never engineered to do that. Its lower premiums reflect that tradeoff precisely.

There is one exception worth knowing about: return-of-premium term life insurance. This type of policy does refund the premiums you paid, but only if you hold the policy through its entire term. Return-of-premium policies carry higher premiums and do not allow any cash surrender before the term ends. So while you might eventually get your money back, you cannot access it early, and you cannot treat it as cash value in the way permanent policies allow.

Here is a concise breakdown of what term life insurance does and does not include:

-

Death benefit protection for a specified term (10, 15, 20, 25, or 30 years are common)

-

No cash value accumulation at any point during the term

-

No dividends or investment component

-

Level premiums in most policies, reflecting the pure protection structure

-

Return-of-premium option available on some policies, but only payable at term end

Pro Tip: Check your policy documents for any riders attached to your term coverage. Some policies include a conversion rider that opens meaningful options, even if the base policy has no cash value.

Options for accessing value from a term policy

Although you cannot directly cash in term life insurance, several alternatives allow you to extract meaningful value depending on your policy type, health status, and financial goals.

Convert to a permanent policy

Conversion is the most widely available option for term life insurance holders who want to shift toward a policy with cash value potential. A conversion rider lets you switch your term policy into a permanent one without submitting to new medical underwriting. Your original health rating is preserved, which is a significant benefit if your health has declined since you first applied.

Once converted, the new permanent policy begins accumulating cash value over time. That cash value can eventually be accessed through policy loans or withdrawals, or the policy itself can be surrendered for its cash surrender value. Conversion does not give you immediate cash, but it starts building access to it.

Sell your policy through a life settlement

This is where term life insurance cash out discussions get more interesting. Under specific conditions, you may be able to sell your term policy to a third-party institutional buyer. Life settlements can provide a lump sum typically ranging from 10% to 25% of the death benefit, and sometimes more depending on the insured’s age, health, and the specific policy terms.

For a term policy to qualify for a life settlement, it generally needs to be convertible. Buyers typically require the ability to convert the policy to permanent coverage so they can maintain it beyond the original term. If your term policy includes a conversion rider and you meet the age and health criteria buyers look for, selling your term life insurance policy may be a legitimate exit strategy.

Cancel or let the policy lapse

The simplest option is also the least financially rewarding. Canceling or allowing a term life policy to lapse results in no payout and no refund unless a return-of-premium rider applies. If your coverage needs have genuinely changed and you have no interest in conversion or settlement, cancellation may be the right administrative choice. But it should be a deliberate decision, not a default outcome.

Here is a side-by-side comparison of the main options:

| Option | Cash received | Medical exam required | Coverage ends |

|---|---|---|---|

| Direct cash out | None | Not applicable | Depends |

| Policy conversion | Delayed (builds over time) | No | No |

| Life settlement | Lump sum (10–25%+ of death benefit) | No (existing records reviewed) | Yes |

| Cancellation or lapse | None (unless return-of-premium) | No | Yes |

Pro Tip: When evaluating a life settlement, work with a licensed broker rather than going directly to a provider. Brokers represent your interests and can solicit competing bids, which typically results in a higher offer.

Tax considerations when cashing out or surrendering

The life insurance cash out tax question trips up many policyholders and their advisors. Whether you are surrendering a permanent policy you converted into, or selling through a life settlement, tax obligations depend on how much you receive relative to what you paid in.

Your cost basis is the total amount of premiums you paid into the policy. Any proceeds above that amount represent a taxable gain. Gains above premiums paid are taxed as ordinary income at your marginal rate, which currently ranges from 10% to 37% depending on total income. This applies whether you receive cash through a surrender or a sale.

There is a less obvious tax risk worth understanding. Constructive receipt rules can trigger a taxable event even if you never receive a check. When a policy with outstanding loans is surrendered, the IRS treats the loan amount offset by the surrender value as income received. This means a policyholder could face a tax bill with no cash in hand to pay it.

A few key points on taxes when cashing out life insurance:

-

Premiums paid form your cost basis and are not taxed upon recovery

-

Gains above cost basis are subject to ordinary income tax, not capital gains rates

-

Policy loans outstanding at the time of surrender are treated as taxable income if they reduce the surrender value

-

Life settlement proceeds above the cost basis are generally taxable as ordinary income or possibly capital gains depending on circumstances

Taxes on cashing out life insurance are not automatic — they depend entirely on the spread between what you paid in and what you receive. Consulting a tax professional before surrendering or selling any life insurance policy is strongly advisable.

Practical steps before changing your term life policy

If you are considering a term life insurance cash out strategy, whether through conversion, sale, or cancellation, a few preparatory steps will save you from costly missteps.

-

Review your conversion privilege. Pull your policy documents and confirm whether a conversion rider exists. Note the conversion deadline carefully. Missing the conversion deadline by even one day eliminates your guaranteed right to convert without medical underwriting. Some insurers tie the deadline to the policy anniversary date; others connect it to your age.

-

Get quotes before converting. If conversion makes sense for your situation, request illustrations from your current insurer and compare them against other permanent policies available through a 1035 exchange. The policy your insurer offers upon conversion may not be the most competitive option in the market.

-

Evaluate life settlement eligibility early. Life settlement buyers consider your age, health status, policy size, and remaining convertibility window. If you are over 65 and have experienced health changes, your policy may qualify. Reach out to a licensed life settlement broker to get a preliminary assessment before making any decisions. Review common mistakes policy owners make so you can avoid the most costly errors in the process.

-

Clarify your financial goals. Are you trying to reduce premium burden? Generate immediate liquidity? Transition coverage? Each goal points to a different solution, and no single option is correct for everyone.

-

Consult both a financial advisor and a tax professional. The interaction between policy decisions, income tax, and estate planning is complex enough that neither discipline should be skipped.

Pro Tip: Ask your insurer directly whether they allow partial conversions. Some carriers will let you convert a portion of the death benefit, which reduces premium cost while preserving some permanent coverage and future cash value potential.

My perspective on the realities of term life cash value misconceptions

I’ve worked with enough policyholders over the years to know that most people who ask about cashing out term life insurance are not asking the wrong question — they are asking the right question too late. The confusion is real, and much of it traces back to how term life insurance is sold. Agents emphasize affordability and coverage amounts. The cash value conversation rarely happens because there is nothing to discuss. But when financial circumstances shift a decade later, policyholders feel blindsided.

What I’ve learned is that the single most overlooked option is conversion. The conversion privilege is often underutilized and frequently misunderstood. Most policyholders don’t know the deadline exists until it has passed. That is a preventable loss. If you have a term policy and you’re even remotely uncertain about whether you’ll need coverage beyond your current term, the time to evaluate conversion is now, not when the deadline is six months away.

I’ve also seen people leave real money on the table by simply letting a convertible term policy lapse when a life settlement would have paid them something meaningful. Selling your policy is not giving up. Sometimes it is the financially sound decision given your current health and coverage needs. Comparing a life settlement to a lapse almost always reveals a significant gap in what you receive.

The one thing I would caution against is treating this as a purely transactional decision. Tax consequences, replacement coverage needs, and long-term financial planning all intersect here. Moving quickly without understanding those dimensions is where costly mistakes happen.

— Brian Hurley

How Accelerated Life Solutions can help

For policyholders who believe their term life insurance may hold more value than a lapse or cancellation would produce, professional guidance makes a measurable difference.

Accelerated Life Solutions specializes in helping policyholders and their advisors evaluate whether a life settlement is the right exit strategy. The team operates independently, which means the focus stays on the policyholder’s financial outcome rather than any provider’s interest. If your term policy is convertible and you meet general eligibility criteria, Accelerated Life Solutions can source competitive bids across the institutional buyer market. Start with the life settlement calculator to get a preliminary estimate of what your policy might be worth, then review real-world life settlement case studies to understand the range of outcomes policyholders have achieved. To discuss your specific situation, contact the team directly for a no-obligation consultation.

FAQ

Can you cash in term life insurance before it expires?

No. Term life insurance has no cash surrender value and cannot be cashed in before the term ends. The policy is designed exclusively to pay a death benefit, not to accumulate accessible cash.

Can you sell your term life insurance policy?

Yes, under specific conditions. If your term policy includes a conversion rider and you meet the age and health criteria, a life settlement allows you to sell the policy to a third-party buyer for a lump sum, typically between 10% and 25% of the death benefit.

Is cashing out a life insurance policy taxable?

Yes, it can be. Any proceeds above your cost basis — the total premiums you paid — are taxed as ordinary income. Gains are subject to your marginal income tax rate, which ranges from 10% to 37%.

What happens if you cancel a term life insurance policy?

Canceling a term life insurance policy ends your coverage with no cash refund, unless your policy includes a return-of-premium rider and has reached its full term. Otherwise, you receive nothing in return for prior premiums paid.

What is a conversion rider and why does it matter?

A conversion rider allows you to switch your term policy to a permanent life insurance policy without a new medical exam. This matters because missing the conversion deadline means losing the guaranteed right to convert, requiring full medical underwriting for any new permanent coverage.