Choosing a life settlement representative is one of the most consequential financial decisions a senior can make when considering selling a life insurance policy. Without the right professional in your corner, you risk accepting far less than your policy is worth or falling victim to unlicensed operators. Sellers who work with qualified brokers receive an average payout more than 6.5 times higher than their policy’s cash surrender value. This guide walks you through every step of finding, evaluating, and working with a trusted representative.

Table of Contents

-

Choosing a life settlement representative: understanding the role

-

My perspective on why this decision deserves more time than most seniors give it

-

How Accelerated Life Solutions can help you find the right representative

Key takeaways

| Point | Details |

|---|---|

| Brokers vs. buyers | A broker represents your interests; a buyer/provider represents institutional investors purchasing your policy. |

| Verify licensing first | Check state insurance department records and FINRA BrokerCheck before engaging any representative. |

| Ask the right questions | Confirm commission rates, offer timelines, data privacy practices, and whether multiple buyers will be approached. |

| Watch for red flags | Unsolicited offers, guaranteed payout promises, and upfront fee requests are warning signs of bad actors. |

| No-cost evaluations exist | Reputable brokers provide a soft-market assessment at no charge, giving you policy value data without commitment. |

Choosing a life settlement representative: understanding the role

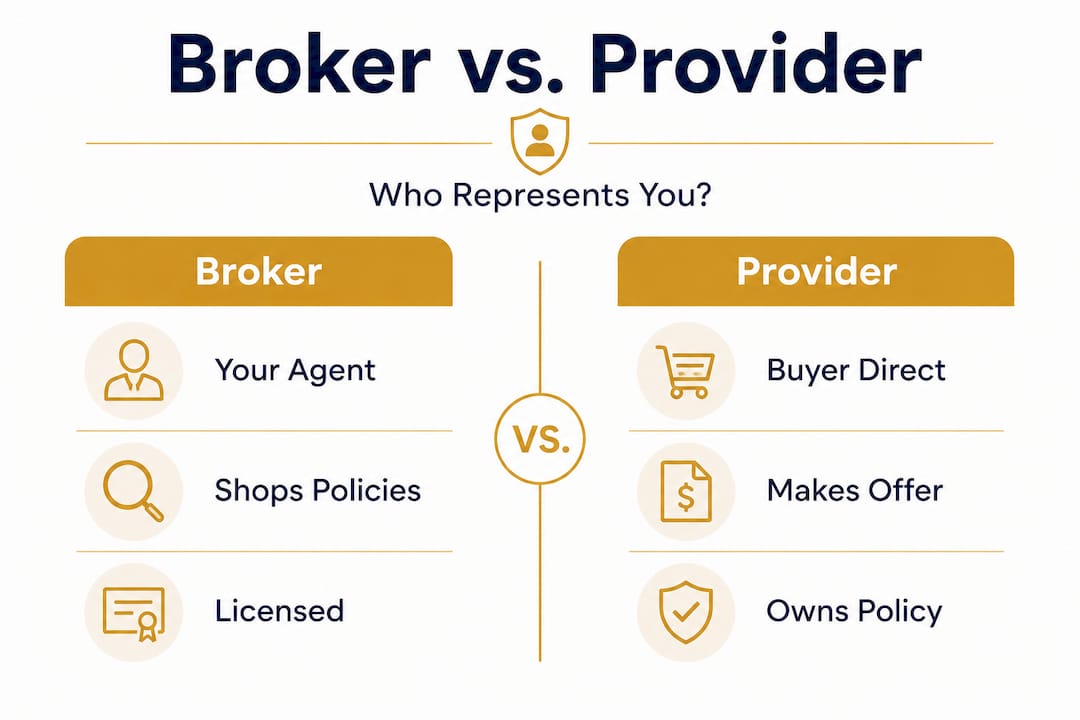

Not all life settlement representatives are the same. The two primary categories are brokers and buyers (also called providers), and the distinction matters significantly for your financial outcome.

A life settlement broker is a licensed professional who represents you, the policyholder. A broker’s legal obligation is to act in your best interest, which is known as a fiduciary duty. A buyer or provider, by contrast, represents the institutional investor purchasing your policy. Their goal is to acquire it at the lowest possible price. Working with a broker rather than going directly to a buyer is generally the more protective choice for sellers.

Brokers are compensated through commissions, typically around 10% of the final life settlement amount. This fee comes from the proceeds of the sale, not from your pocket upfront. Buyers do not charge sellers fees, but their interests are fundamentally misaligned with yours.

Here is what a licensed life settlement broker does on your behalf:

-

Conducts a no-cost soft-market assessment to estimate your policy’s value

-

Runs a competitive auction among buyers to generate multiple simultaneous offers

-

Handles documentation, compliance, and regulatory requirements

-

Explains each offer clearly and helps you compare terms

-

Advocates for the highest possible payout throughout negotiations

Pro Tip: Ask any representative you speak with to confirm in writing whether they are acting as a broker (representing you) or a provider (representing a buyer). This single question clarifies whose interests they are legally obligated to protect.

The life settlement market is regulated in 43 U.S. states, which means licensing requirements and consumer protections vary by location. States without life settlement regulations present higher risks for consumers, making it even more critical to verify credentials before proceeding.

Credentials and criteria to verify before hiring

Once you understand the difference between a broker and a buyer, the next step is verifying that any representative you consider is properly licensed and operating ethically. This process does not need to be complicated, but it does require some deliberate research.

Follow these steps in order before committing to any representative:

-

Check state licensing. Contact your state’s insurance department to confirm the representative holds a valid life settlement broker license. Licensing requirements differ by state, so this step is non-negotiable.

-

Use FINRA BrokerCheck. If the representative is also a registered financial advisor, verify credentials using FINRA’s BrokerCheck to review their disciplinary history and registration status.

-

Confirm LISA membership. Reputable life settlement companies often maintain membership in the Life Insurance Settlement Association (LISA), which enforces a strict code of ethics that members confirm annually. LISA membership is a meaningful quality marker.

-

Request fee and commission disclosures. A trustworthy broker will provide clear, written disclosure of their commission structure before you sign anything. Vague or evasive answers about compensation are a warning sign.

-

Review their professional reputation. Search the representative’s name and company through the Better Business Bureau and read consumer reviews on independent platforms. Look for patterns in complaints, not just isolated negative reviews.

-

Confirm fiduciary status in writing. Ask directly whether they are legally obligated to act in your best interest. A genuine fiduciary will confirm this without hesitation.

Pro Tip: Request a sample engagement letter or service agreement before committing. A reputable broker will provide one readily. Review it for clear language on commission rates, the number of buyers they will approach, and your right to decline any offer.

| Verification step | What to look for |

|---|---|

| State insurance license | Active license with no disciplinary actions |

| FINRA BrokerCheck | Clean registration record if dually licensed |

| LISA membership | Current, confirmed annual ethics commitment |

| Fee disclosure | Written commission rate before engagement |

| BBB and reviews | Consistent positive feedback, resolved complaints |

Financial planning expert Alex Barba emphasizes treating life insurance as a marketable asset requiring periodic valuation. That perspective reinforces why the representative you choose should approach your policy with the same rigor as any other financial asset.

Questions to ask life settlement representatives

Gathering credentials is the foundation. Asking the right questions is what separates a good decision from a great one. These questions to ask life settlement representatives will help you assess their experience, process, and commitment to your interests.

Before signing any agreement, ask each candidate representative the following:

-

How many life settlement transactions have you completed, and how long have you been in this business? Experience matters. A representative with a multi-year track record and documented transactions is far more reliable than someone new to the field.

-

How many buyers will you approach with my policy? A broker who contacts only one or two buyers is not running a true competitive process. You want someone who reaches a broad pool of institutional buyers simultaneously.

-

What is your exact commission rate, and are there any additional fees? Reputable brokers disclose commission structures clearly and do not pressure sellers. You should never pay anything out of pocket upfront.

-

How do you protect my personal and medical information? Life settlement transactions require sensitive data. Ask specifically about data security protocols, who has access to your information, and how long it is retained.

-

What is the typical timeline from application to receiving funds? Timelines vary, but a knowledgeable representative should give you a realistic range based on your policy type and health status.

-

Can you share case studies or examples of outcomes for clients with similar policies? Concrete examples from real policyowner outcomes demonstrate competence and give you a realistic sense of what to expect.

Pro Tip: If a representative becomes evasive or impatient when you ask these questions, treat that as a disqualifying signal. A professional who genuinely represents your interests will welcome thorough inquiry.

Reputable firms also allow you to change your mind. Clients can withdraw within 15 days of the life settlement date with no penalty at well-run operations. Confirm this policy before you engage.

Red flags and pitfalls to avoid

Knowing what a good representative looks like is only half the picture. Recognizing the warning signs of a bad one is equally important. The life settlement market, while heavily regulated in most states, still attracts bad actors who target seniors.

Watch for these specific red flags when picking a life settlement agent:

-

Unsolicited contact. If someone contacts you out of the blue offering to buy your policy or connect you with buyers, proceed with extreme caution. Legitimate representatives do not typically cold-call seniors with life settlement offers.

-

Guaranteed high payouts. No honest representative can guarantee a specific life settlement amount before reviewing your policy details and running a market assessment. Guaranteed numbers are a manipulation tactic.

-

Pressure to decide quickly. Any representative who creates artificial urgency or discourages you from seeking a second opinion is not operating in your interest. Take the time you need.

-

Unlicensed operations. States without life settlement regulations pose higher risks for consumers, and unlicensed representatives can operate in regulatory gray areas. Always verify licensing through your state insurance department.

-

Requests for upfront fees. Legitimate brokers collect commissions from the life settlement proceeds, not from you in advance. Any request for payment before a transaction is completed should stop the conversation immediately.

-

Vague or missing credentials. If a representative cannot provide their license number, association memberships, or written disclosures promptly, that absence of transparency is itself a red flag.

Experts recommend careful due diligence as a core best practice for avoiding legal and financial risks when selling a life insurance policy. If you have any doubt about a representative’s legitimacy, consult an independent attorney or financial advisor before proceeding.

What to expect after choosing a representative

Once you have selected a qualified representative, understanding the process ahead helps you stay informed and engaged throughout the transaction.

Here is a general sequence of what happens after you engage a licensed broker:

-

Soft-market assessment. Most seniors do not realize that a broker provides this evaluation at no cost. The broker reviews your policy details and health information to estimate market value before any formal offers are made. You are under no obligation to proceed.

-

Policy documentation. You will provide your policy documents, recent statements, and medical records. The broker handles the submission to buyers on your behalf.

-

Competitive bidding. The broker submits your policy to multiple institutional buyers simultaneously. This competitive process is what drives higher offers.

-

Offer review and comparison. You receive all offers in writing. Your broker explains the terms of each and provides a clear recommendation, but the decision is always yours.

-

Negotiation. Your broker negotiates on your behalf to improve terms where possible.

-

Closing and transfer. Once you accept an offer, the broker manages the closing paperwork and policy transfer. Funds are typically held in escrow until all conditions are met.

| Stage | Typical timeframe |

|---|---|

| Soft-market assessment | 1 to 2 weeks |

| Documentation and submission | 2 to 4 weeks |

| Bidding and offer receipt | 4 to 8 weeks |

| Closing and fund transfer | 2 to 4 weeks after acceptance |

After the sale closes, review the tax implications with your accountant. Life settlement proceeds may be partially taxable depending on your policy’s cost basis, and a qualified tax professional can help you plan accordingly.

My perspective on why this decision deserves more time than most seniors give it

I have worked in the life settlement sector long enough to see the same mistake repeated: seniors make this decision too quickly, often because they feel financial pressure or because the first representative they spoke with seemed confident and friendly. Confidence and friendliness are not credentials.

What I have seen consistently is that the seniors who get the best outcomes are the ones who treat this process the way they would treat hiring an attorney or selecting a surgeon. They ask hard questions. They verify licenses. They get second opinions. They do not sign anything until they understand every term.

The misconception I encounter most often is that all life settlement representatives are essentially the same. They are not. A broker who contacts 20 institutional buyers will almost always generate a higher offer than one who contacts three. A fiduciary who discloses their commission upfront operates in a fundamentally different way than one who buries that information in fine print.

I also want to be direct about something that rarely gets said plainly: a fiduciary advisor’s role includes proactively raising the option of a life settlement during annual reviews. If your financial advisor has never mentioned this possibility, that is worth a conversation. You may be sitting on an asset with significant market value that no one has told you about.

Take the time this decision deserves. Use the resources available to you. And do not let urgency, real or manufactured, push you into a choice you have not fully evaluated.

— Brian Hurley

How Accelerated Life Solutions can help you find the right representative

Accelerated Life Solutions operates as an independent life settlement broker, which means the firm represents policyowners, not institutional buyers. Accelerated Life Solutions reaches a broad pool of competitive buyers simultaneously, running the kind of structured bidding process that consistently generates stronger offers than direct-to-buyer transactions.

For seniors exploring their options, Accelerated Life Solutions offers a free life settlement calculator to estimate your policy’s potential market value with no commitment required. The firm’s team provides personalized consultations, transparent commission disclosures, and clear guidance at every stage of the process. To speak with a licensed representative or learn more about how the process works, contact Accelerated Life Solutions directly. Every conversation starts with education, not a sales pitch.

FAQ

What does a life settlement broker do for the seller?

A life settlement broker is a licensed fiduciary who represents the policyholder, not the buyer. The broker markets your policy to multiple institutional buyers simultaneously to generate competitive offers and maximize your payout.

How do I verify a life settlement representative’s credentials?

Check your state insurance department for an active life settlement broker license, use FINRA BrokerCheck if the representative is also a financial advisor, and confirm membership in LISA, which enforces an annual code of ethics.

Are there any upfront costs when working with a life settlement broker?

Reputable brokers do not charge upfront fees. Their commission, typically around 10% of the life settlement amount, is paid from the proceeds of the sale after the transaction closes.

What is a soft-market assessment?

A soft-market assessment is a no-cost, no-commitment evaluation that a licensed broker provides to estimate your policy’s market value before formally approaching buyers. It gives you useful data without any obligation to proceed.

How long does the life settlement process typically take?

From the initial assessment through closing, the process generally takes between two and four months, depending on policy complexity, documentation requirements, and the number of buyers participating in the bidding process.