When you sell a life insurance policy through a life settlement, the tax implications can feel more complicated than the transaction itself. Many policyowners who receive Form 1099-LS assume it means a large tax bill is coming, but that assumption often overstates the actual liability. Life settlements and taxes 1099 LS reporting follow a structured federal framework, and understanding how proceeds are classified across multiple tiers can dramatically change your outlook. This guide breaks down exactly how the IRS views your settlement proceeds, what the forms mean, and how to approach reporting with confidence.

Table of Contents

- Key Takeaways

- What a life settlement is and how it differs from surrender

- Understanding Form 1099-LS and its filing requirements

- The three-tier federal tax framework on settlement proceeds

- Reconciling Form 1099-LS and Form 1099-SB

- Special considerations: viatical settlements and state taxes

- My perspective on navigating life settlement taxes

- How Accelerated Life Solutions can help

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| 1099-LS reports gross proceeds | The form shows total settlement proceeds, not your taxable amount. |

| Three-tier tax framework applies | Proceeds are split into tax-free return of basis, ordinary income, and capital gains. |

| Viatical settlements may be tax-free | Qualifying terminally ill policyowners can exclude proceeds under IRC § 101(g). |

| Two forms must be reconciled | Both 1099-LS and 1099-SB are needed to calculate your actual taxable gain. |

| State taxes vary by location | Your state of residence can significantly affect the total tax owed on proceeds. |

What a life settlement is and how it differs from surrender

A life settlement is the sale of an existing life insurance policy to a third-party buyer for a lump-sum payment that exceeds the policy's cash surrender value but falls below the face value death benefit. The buyer takes over premium payments and collects the death benefit when the insured passes. This process is regulated at the state level and involves licensed brokers and institutional buyers.

Surrendering a policy, by contrast, means returning it directly to the insurance carrier in exchange for its accumulated cash surrender value. The difference between settlement and surrender is financially significant. Surrender values are fixed by the insurer and typically reflect a fraction of the policy's actual market worth. A life settlement surfaces competitive bids from multiple buyers, often returning two to four times the surrender amount.

Policyowners consider life settlements for several reasons:

- Premium payments have become unaffordable

- The policy no longer fits current estate planning or income goals

- The insured no longer needs the coverage

- Liquidity is needed for long-term care, retirement expenses, or medical costs

Pro Tip: Before accepting a surrender offer from your insurer, request a life settlement evaluation. The open market consistently produces higher proceeds, and understanding the gap helps you make an informed decision.

The tax treatment of those higher proceeds is where the complexity begins. Because the settlement produces a payment above what you put in, the IRS wants to understand how much of that payment is a recovery of your own money versus a gain.

Understanding Form 1099-LS and its filing requirements

Form 1099-LS is the IRS document that officially records a reportable life insurance policy sale. The IRS requires the acquirer to file this form when they purchase a life insurance contract in a reportable policy sale. That means the buyer, not the seller, is responsible for filing the form and sending a copy to you as the policyowner.

The form captures the gross amount paid to you for your policy. It does not reflect your tax basis, your cost of premiums, or your actual taxable gain. This is a critical distinction that causes a lot of unnecessary anxiety.

Here is what Form 1099-LS typically includes:

- Box 1: Gross proceeds paid to the policyowner

- Box 2: Date of sale

- Issuer information: Name and contact details of the buyer or acquirer

- Seller information: Your name, address, and taxpayer identification number

The filing requirements fall under IRC Section 6050Y, which was added by the Tax Cuts and Jobs Act of 2017. This law created a formal reporting structure for life settlement transactions that did not previously exist in this standardized form.

Receiving a 1099-LS triggers IRS reporting, but it does not by itself determine how much you owe. That calculation requires additional data from your policy records and, in most cases, a second IRS form.

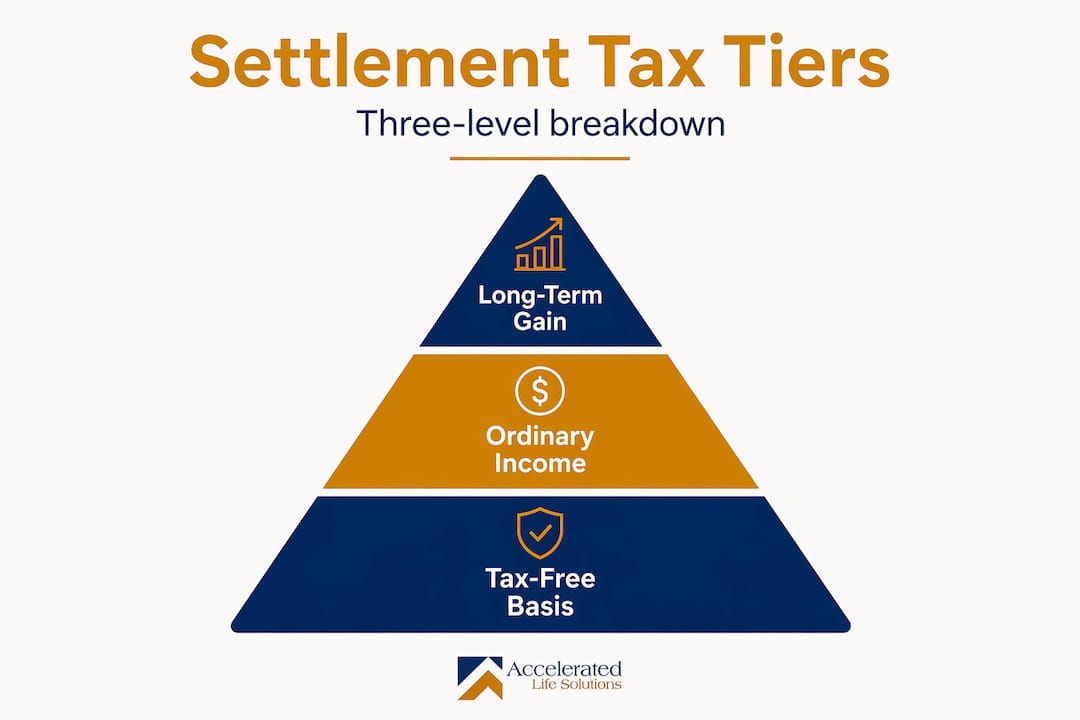

The three-tier federal tax framework on settlement proceeds

The federal tax treatment of life settlement proceeds follows a three-tier framework that breaks the gross settlement amount into distinct tax categories. Each tier carries a different tax rate, and the split between them depends entirely on your policy's specific tax basis and cash surrender value at the time of sale.

Here is how the tiers work with a practical example. Assume you sell a policy for $200,000. Your cumulative premiums paid (your tax basis) total $80,000, and the policy's cash surrender value at sale is $110,000.

| Tier | Amount | Tax Treatment |

|---|---|---|

| Return of basis | $0 to $80,000 | Tax-free |

| Ordinary income | $80,001 to $110,000 | Taxed at ordinary income rates |

| Capital gains | $110,001 to $200,000 | Taxed at long-term capital gains rates |

In this example, $80,000 is returned to you tax-free, $30,000 is taxed as ordinary income, and $90,000 is taxed as long-term capital gains. The tax character of each portion depends on those two internal policy valuations: your basis and the cash surrender value.

The Tax Cuts and Jobs Act of 2017 eliminated the requirement to reduce your tax basis by historical cost-of-insurance charges. This change increased many policyowners' tax basis, which in turn reduced their taxable gain. If you sold a policy before 2018 and were told your basis was lower, it may be worth revisiting those calculations under current rules.

One less discussed scenario: if you sell the policy below your tax basis, the transaction generates a capital loss deductible against other capital gains or up to $3,000 of ordinary income per year.

Pro Tip: Ask your insurer for the official cash surrender value on the date of sale. This specific figure, not an estimate, determines how much of your gain falls into the ordinary income tier versus the more favorably taxed capital gains tier.

Reconciling Form 1099-LS and Form 1099-SB

Most policyowners involved in a life settlement will receive two separate IRS forms for the same transaction. Both forms are needed to calculate taxable income accurately, and misunderstanding either one can lead to errors on your tax return.

Form 1099-LS, as explained earlier, reports the gross proceeds paid by the buyer. Form 1099-SB is filed by the insurance carrier and reports your investment in the contract, which is your tax basis. The two forms together provide the data set required for the three-tier tax calculation.

Key points to understand when working with both forms:

- 1099-LS: Issued by the buyer (acquirer); reports gross sale price

- 1099-SB: Issued by the insurance company; reports your adjusted tax basis

- Your taxable gain: Calculated as gross proceeds minus tax basis, then further divided into ordinary income and capital gains using the cash surrender value

- Errors are possible: Insurance carriers sometimes report an incorrect basis, particularly for older policies or policies that have been exchanged or modified over time

If the figures on your 1099-SB do not match your own records of premiums paid, address that discrepancy before filing your return. The insurer can issue a corrected form if the reported basis is demonstrably wrong.

Pro Tip: Keep a complete record of every premium payment made over the life of your policy. This documentation is your defense against an understated basis on the 1099-SB and directly reduces your taxable gain.

Reconciling these forms is not intuitive for most taxpayers. A tax professional who has experience with life insurance settlement taxes is worth consulting, especially for policies with complex histories involving loans, exchanges, or riders.

Special considerations: viatical settlements and state taxes

Not all life settlement proceeds are taxed equally. Several factors can change the tax picture significantly, and being aware of them may reveal an outcome much more favorable than the standard framework suggests.

-

Viatical settlement exclusion. If you are terminally ill with a life expectancy of 24 months or less, proceeds from a qualifying viatical settlement are excluded from gross income under IRC § 101(g). This federal exclusion applies regardless of the settlement amount, making it one of the most significant tax benefits available to policyowners facing serious illness. The key requirement is that the sale must go through a licensed viatical settlement provider.

-

State income tax treatment. Federal rules are only part of the picture. State tax treatments vary widely, with some states like Florida, Texas, and Alaska imposing no personal income tax at all. States like California and New York tax life settlement gains similarly to federal rules. Washington state applies a capital gains excise tax. Your state of residence at the time of sale determines which rules apply, and in some cases that decision alone can affect your net proceeds by tens of thousands of dollars.

-

Net Investment Income Tax. The capital gains portion of your settlement proceeds may also be subject to the 3.8% Net Investment Income Tax if your modified adjusted gross income exceeds certain thresholds ($200,000 for single filers; $250,000 for married filing jointly). This is often overlooked when estimating after-tax proceeds.

-

Death benefit proceeds. If you are a beneficiary receiving proceeds after the insured has passed, those death benefits are generally excluded from taxable income under federal rules. However, any interest earned on those proceeds is taxable. Policies transferred for value before death may lose part or all of this exclusion.

Tax treatment also changes depending on why life insurance qualifies as a retirement or planning asset, particularly when structured with tax-deferred accumulation features that interact with settlement proceeds.

The variation across these scenarios is the reason personalized tax advice matters so much. No two policies produce identical tax outcomes.

My perspective on navigating life settlement taxes

I've worked with enough policyowners to know that Form 1099-LS causes more stress than it should. People see a large number in Box 1 and immediately assume they owe taxes on the entire amount. That assumption is almost never correct.

What I've learned is that the most common mistake isn't filing the wrong form. It's not knowing your policy's tax basis before you accept a settlement offer. If you understand your basis and your cash surrender value going in, you can estimate your tax tiers with reasonable accuracy and factor that into your decision. Too many people find out about the tax implications after they've already signed.

I've also seen situations where 1099-SB figures were wrong by significant amounts, and taxpayers accepted them without question. That can cost you real money. Always cross-reference the basis on the 1099-SB against your own premium payment records.

My strongest recommendation: don't let an unfamiliar tax form keep you from exploring a life settlement if you have a policy you no longer need. The proceeds, even after taxes, frequently exceed what you'd receive from surrendering the policy. Work with a broker who understands the process and a tax professional who has handled life settlement reporting before. The combination of those two relationships makes the entire process far more manageable than it looks on paper.

— Brian Hurley

How Accelerated Life Solutions can help

If the tax and reporting details covered in this article feel like a lot to manage on your own, that's exactly where having the right partner matters.

Accelerated Life Solutions works with policyowners and fiduciaries to evaluate policies, surface competitive market offers, and provide the kind of transparent guidance that makes informed decisions possible. You can use the life settlement calculator to get an initial estimate of your policy's market value. For a closer look at real outcomes, the case studies on the Accelerated Life Solutions website show how policyowners in different situations navigated both the financial and tax dimensions of their settlements. To discuss your policy directly with an experienced advisor, visit the Accelerated Life Solutions broker page and request a consultation.

FAQ

What is Form 1099-LS used for?

Form 1099-LS reports the gross proceeds paid to a policyowner in a reportable life insurance policy sale. It is filed by the buyer of the policy and sent to both the seller and the IRS under IRC Section 6050Y.

Are life settlement proceeds fully taxable?

No. Life settlement proceeds are divided into three tiers: a tax-free return of your premium basis, an ordinary income portion up to the cash surrender value, and a capital gains portion above that. Only the second and third tiers generate a tax liability.

Why do I receive both a 1099-LS and a 1099-SB?

The 1099-LS and 1099-SB together provide the two data points needed to calculate your taxable gain. The 1099-LS shows what you were paid; the 1099-SB shows your tax basis in the policy.

Are viatical settlement proceeds taxable?

Proceeds from a qualifying viatical settlement received by a terminally ill insured are excluded from federal gross income under IRC § 101(g). The insured must have a life expectancy of 24 months or less, and the sale must involve a licensed provider.

Do state taxes apply to life settlement proceeds?

Yes, in most states. State tax treatment varies significantly, from no income tax in states like Florida and Texas to full capital gains taxation in states like California. Consulting a tax advisor familiar with your state's rules is recommended before completing a sale.