Not every life insurance policy is a strong candidate for a life settlement, and that distinction matters more than most policyowners realize. Understanding why whole life policies qualify for settlements requires looking at what settlement buyers actually want: contractual certainty, measurable cash value, and permanent coverage that does not expire. Whole life insurance delivers all three. This article breaks down the structural and financial reasons whole life policies consistently meet settlement eligibility criteria, clears up common misconceptions, and outlines practical steps for policyowners and financial advisors exploring this option.

Table of Contents

-

My perspective on whole life settlements in financial planning

-

How Accelerated Life Solutions can help you explore settlement options

Key takeaways

| Point | Details |

|---|---|

| Permanent coverage is the key | Whole life policies never expire, giving settlement buyers the contractual certainty they require. |

| Cash value signals policy strength | Guaranteed cash value growth makes whole life policies more attractive and easier to value than term policies. |

| Eligibility has clear thresholds | Most policyowners qualify if they are 65 or older with a policy death benefit of at least $100,000. |

| Settlements often beat surrenders | A life settlement can return significantly more than the policy’s cash surrender value. |

| Advisors carry a planning duty | Financial professionals have an obligation to discuss settlement options before a client lapses or surrenders a policy. |

Why whole life policies qualify for settlements

A life settlement is the sale of an existing life insurance policy to a third-party buyer for a lump sum greater than the policy’s cash surrender value but less than the death benefit. The buyer takes over premium payments and collects the death benefit when the insured passes. For this transaction to work, the buyer needs to evaluate the policy’s value with confidence.

That confidence comes from specific eligibility factors. Typical criteria include age 65 or older and a minimum death benefit of $100,000. Younger individuals with serious medical conditions may also qualify. Health status, life expectancy, and policy structure all factor into the underwriting review.

Here is where whole life policies have a clear structural advantage over term policies:

-

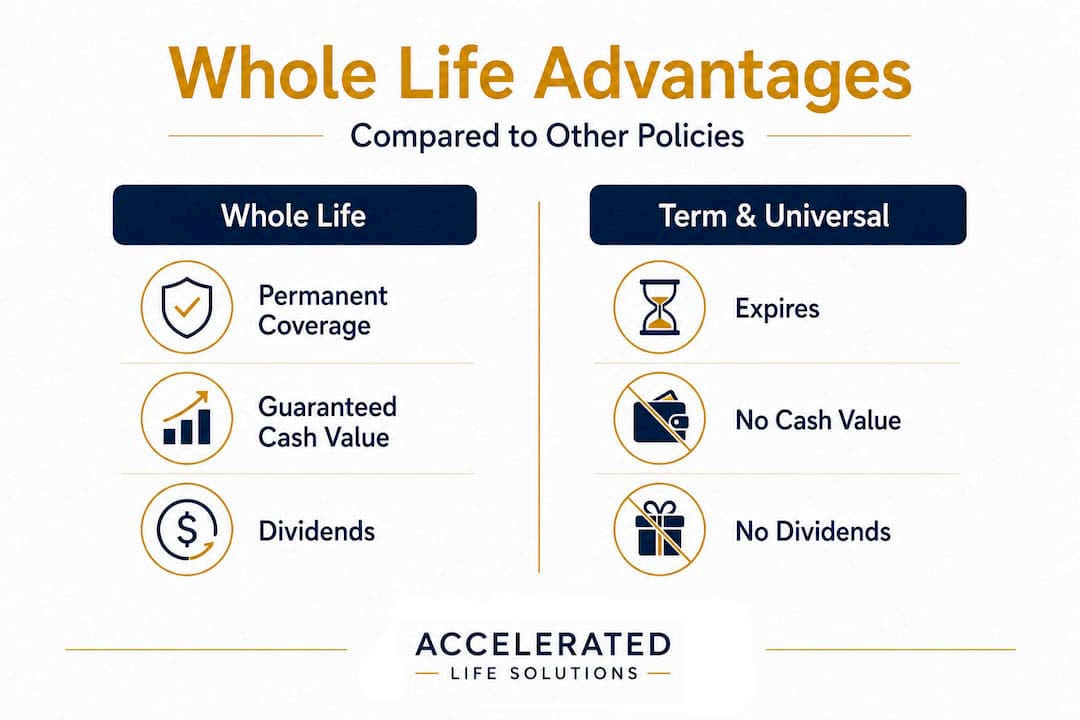

Permanent coverage: Whole life policies do not expire. Term policies do. A buyer purchasing a term policy risks the coverage lapsing before the insured passes, which destroys the investment.

-

Cash value: Whole life policies accumulate cash value over time. This gives buyers a measurable floor on the asset’s worth.

-

Predictable premiums: Whole life premiums are fixed. Buyers can calculate future premium obligations with precision.

-

Contractual guarantees: The death benefit and cash value growth are contractual, not market-dependent.

The underwriting process for settlements involves medical records, family history, and lifestyle analysis to determine life expectancy. A shorter life expectancy generally produces a higher offer, because the buyer expects to collect the death benefit sooner. This is a critical point for policyowners to understand before entering the process.

Structural and financial reasons whole life qualifies

The structural features of whole life insurance are not incidental. They are the reason settlement buyers prefer these policies over nearly every other type.

Permanent policies have residual cash value that investors can evaluate, unlike term policies which expire without value. This distinction drives the entire settlement market’s preference for whole life and, in many cases, universal life insurance.

The table below compares how the three main policy types perform against typical settlement qualification criteria:

| Feature | Whole life | Universal life | Term life |

|---|---|---|---|

| Permanent coverage | Yes | Yes | No |

| Cash value | Guaranteed | Variable/flexible | None |

| Premium predictability | Fixed | Flexible (risk of lapse) | Fixed but temporary |

| Settlement eligibility | High | Moderate to high | Low to none |

| Actuarial certainty for buyers | Very high | Moderate | Very low |

Universal life policies can qualify for settlements, though the picture is more complex. Why universal life policies often qualify for settlements relates to their permanent coverage feature, but the flexible premium structure introduces lapse risk that buyers must account for. A universal life policy that has not been properly funded may have a depleted cash value, which reduces its attractiveness to buyers.

Whole life policies carry none of that ambiguity. Cash value is a contractual obligation, not a market projection. Dividends from participating whole life policies can further enhance the cash value, adding another layer of measurable value that settlement buyers factor into their offers.

Whole life policies are actuarially priced with guaranteed cash values independent of market conditions. This makes them highly reliable assets in the secondary market. A buyer purchasing a whole life policy knows exactly what the floor value is today and can model future premium costs with precision. That level of certainty simply does not exist with term or poorly funded universal life policies.

Pro Tip: If you are a financial advisor reviewing a client’s policy portfolio, check whether any whole life policies have significant accumulated cash value. Those policies are the strongest candidates for settlement discussions and should be evaluated before any lapse or surrender decision is made.

Common misconceptions about whole life settlements

Not every whole life policy is a strong settlement candidate, and assuming otherwise can lead to poor decisions. Several misconceptions persist in this space that policyowners and advisors should address directly.

The first misconception is that any whole life policy will generate a lucrative settlement offer. Policy size matters significantly. A $50,000 death benefit policy is unlikely to attract competitive bids from institutional buyers who operate at scale. The economics of the underwriting process favor larger policies.

The second misconception is that the settlement process is unregulated and risky by nature. In reality, 43 states regulate life settlement transactions, providing meaningful consumer protections. That said, regulatory coverage does not eliminate all risk.

FINRA warns that life settlements involve selling a financial interest tied to the insured’s death, and cautions consumers to be alert to aggressive sales tactics, particularly those targeting seniors. Always work with licensed, regulated brokers and verify credentials before proceeding.

Additional points to consider before pursuing a settlement:

-

Tax implications: Settlement proceeds may be partially taxable. Consult a tax advisor before finalizing any transaction.

-

Medicaid eligibility: A lump sum from a settlement could affect means-tested benefit eligibility.

-

Beneficiary impact: The death benefit will transfer to the buyer, removing it from the estate.

-

Policy loans outstanding: Existing loans against the cash value will reduce the net settlement proceeds.

There are also situations where surrendering a policy may be the more practical choice. If a policy has a very high cash surrender value relative to the likely settlement offer, or if the policyowner is in excellent health (which lowers settlement offers), the surrender route may produce comparable results with less complexity.

Steps to take when considering a settlement

For policyowners and advisors ready to explore whole life insurance settlements, the process follows a clear sequence. Moving through each step methodically protects the policyowner’s interests and produces more competitive offers.

-

Confirm basic eligibility. Review the insured’s age, health status, and policy death benefit. The standard threshold is age 65 with a minimum $100,000 death benefit, though exceptions exist for younger individuals with significant health conditions.

-

Gather policy documentation. Collect the policy contract, premium payment history, current cash value statements, and any outstanding loan balances. Buyers will request all of this during underwriting.

-

Obtain medical records. The settlement underwriting process requires a detailed health review. Prepare authorization forms for medical record release to streamline the process.

-

Work with a licensed life settlement broker. A broker represents the policyowner’s interests and submits the policy to multiple buyers to generate competing offers. This competition is what drives offer values above the surrender value.

-

Use a settlement calculator for initial estimates. Tools like the life settlement calculator at Accelerated Life Solutions provide a quick preliminary estimate of potential value before committing to a full underwriting submission.

-

Evaluate offers carefully. Compare each offer against the policy’s current surrender value, outstanding premiums, and the policyowner’s financial needs. Consider the tax treatment of each offer.

-

Review the impact on estate planning. Removing a death benefit from an estate changes the liquidity picture for heirs. Advisors should model the estate impact before the policyowner accepts any offer.

Pro Tip: Life expectancy is the single largest driver of settlement offer value. Understanding how life expectancy influences valuations before submitting a policy for review helps advisors set realistic expectations with clients and avoid surprises during the offer phase.

Benefits of settling a whole life policy

The financial case for exploring a life settlement before surrendering or lapsing a whole life policy is well documented. The benefits extend to both policyowners and the advisors serving them.

For policyowners, the primary advantages include:

-

Proceeds above surrender value. A settlement offer typically exceeds the cash surrender value because buyers are paying for the future death benefit, not just the current cash value. In documented cases, settlements returned several times the surrender value, converting $38,000 in annual premiums into immediate liquidity.

-

Elimination of premium obligations. Once the policy is sold, the policyowner stops paying premiums. For seniors on fixed incomes, this relief can be significant.

-

Immediate liquidity. Settlement proceeds can fund retirement expenses, long-term care costs, or other financial priorities without requiring the policyowner to take on debt.

-

Estate planning flexibility. Proceeds can be redirected into other estate planning vehicles that better match current goals.

For financial advisors, the benefits are equally concrete. Fiduciary advisors have a duty to discuss life settlements when clients are considering lapsing or surrendering policies. Failing to raise the settlement option when it could produce superior financial outcomes creates both an ethical gap and potential liability exposure. Proactively including settlement reviews in annual policy audits demonstrates thoroughness and builds client trust.

It is also worth noting that policy loans against whole life cash value offer a tax-free alternative to accessing funds, but they accrue interest and reduce the death benefit if unpaid. A settlement, by contrast, provides a clean exit with no ongoing obligations.

My perspective on whole life settlements in financial planning

I have watched advisors walk clients through policy surrenders without once raising the settlement option, and it is one of the most preventable financial mistakes I see in this industry. The conversation is not complicated. The question is simply whether the advisor knows to ask it.

What I have found is that the resistance often comes from unfamiliarity, not from a deliberate choice to withhold information. Many advisors were never trained to think of a life insurance policy as a secondary market asset. But that is exactly what a whole life policy is, particularly one with a substantial death benefit and years of accumulated cash value.

The advisor’s guide to life settlements I recommend to every financial professional in this space makes one point that I return to repeatedly: a policy that is about to lapse has zero value to the client. A settlement offer, even a modest one, is infinitely better than zero. The math is not subtle.

My view is that the fiduciary standard demands this conversation. Not as an optional add-on, but as a standard part of any policy review for clients over 65 with permanent policies. The settlement market is regulated, competitive, and capable of producing outcomes that genuinely change a client’s financial position in retirement. Skipping that conversation is not neutral. It is a missed opportunity that the client may never recover.

— Brian Hurley

How Accelerated Life Solutions can help you explore settlement options

If you or your client holds a whole life policy that is no longer serving its original purpose, the next step is a structured evaluation, not a surrender form. Accelerated Life Solutions works exclusively with financial professionals and their clients to assess policy value, source competitive offers from institutional buyers, and manage the settlement process from submission to close.

Start with the settlement value estimator to get a preliminary read on what a policy might be worth in the secondary market. For policies that meet initial thresholds, the Accelerated Life Solutions broker services team manages the full underwriting and offer process, protecting the policyowner’s interests at every stage. Review real policyowner outcomes in the settlement case studies to understand what results are realistic before committing to any path.

FAQ

What makes a whole life policy eligible for a life settlement?

Whole life policies qualify primarily because they offer permanent coverage, guaranteed cash value, and fixed premiums. Most policyowners are eligible if they are 65 or older with a death benefit of at least $100,000.

How does a settlement compare to surrendering a whole life policy?

A life settlement typically produces a higher payout than the cash surrender value because buyers are purchasing the future death benefit, not just the current cash value. In documented cases, settlement proceeds have exceeded surrender values by a substantial margin.

Do universal life policies also qualify for settlements?

Yes. Why universal life policies often qualify for settlements comes down to their permanent coverage feature. However, flexible premium structures can introduce lapse risk, which may reduce a policy’s attractiveness to buyers compared to a fully funded whole life policy.

What are the risks of a life settlement?

Risks include potential tax liability on proceeds, impact on Medicaid eligibility, removal of the death benefit from the estate, and the ethical complexity of a third party holding a financial interest tied to the insured’s death. FINRA advises consumers to work only with licensed, regulated brokers.

Should a financial advisor always discuss life settlements with clients?

Financial advisors operating under a fiduciary standard have an ethical obligation to discuss life settlements whenever a client is considering lapsing or surrendering a permanent policy. Failing to raise the option when it could produce a better financial outcome represents a gap in the advisor’s duty of care.