A life settlement is defined as the sale of an existing life insurance policy to a third-party investor for a lump-sum cash payment that exceeds the policy’s cash surrender value but is less than its death benefit. The buyer assumes all future premium obligations and collects the death benefit when the insured passes away. For policyowners aged 65 and older who no longer need or can afford their coverage, this transaction can convert an underperforming asset into meaningful liquidity. Regulated brokers, fiduciary advisors, and institutions like Mutual of Omaha recognize life settlements as a legitimate financial planning tool, not a fringe option.

What is a life settlement and how does it work?

A life settlement contract transfers ownership of a life insurance policy from the original policyowner to a third-party buyer in exchange for an immediate cash payment. The seller walks away with cash. The buyer takes over premium payments and eventually receives the death benefit. This structure benefits both parties: the seller gains liquidity today, and the buyer profits over time.

The process follows a clear sequence:

-

The policyowner contacts a licensed life settlement broker to assess eligibility.

-

The broker gathers policy documents, medical records, and life expectancy data.

-

Multiple institutional buyers submit competing offers.

-

The seller reviews offers, selects one, and completes the transfer of ownership.

-

Funds are delivered, typically through escrow-style controls, to protect both parties.

Life settlements are distinct from viatical settlements. A viatical settlement applies specifically to terminally ill policyholders facing imminent death. A life settlement, by contrast, serves policyowners who are not in a health crisis but for whom continuing coverage no longer aligns with their financial goals. The legal foundation for this distinction traces back to Grigsby v. Russell (1911), which established life insurance policies as transferable personal property.

Life settlement underwriting factors explained

Offer size is not arbitrary. Actuarial assessments of life expectancy and policy economics drive pricing, meaning buyers calculate how long they expect to pay premiums before collecting the death benefit. A shorter life expectancy generally produces a higher offer. Health changes, including new diagnoses or declining functional status, can materially increase what buyers are willing to pay.

Eligibility criteria typically require the insured to be age 65 or older, hold a permanent policy with a minimum face value of $100,000, and have maintained the policy in force for a sufficient duration. Universal life, whole life, and certain convertible term policies often qualify. Understanding why whole life policies qualify can help heirs and policyowners assess their options before assuming a policy has no secondary market value.

Pro Tip: Request a life expectancy report from an independent medical underwriter before approaching the market. Buyers use these reports to price offers, and knowing your baseline helps you evaluate whether an offer is competitive.

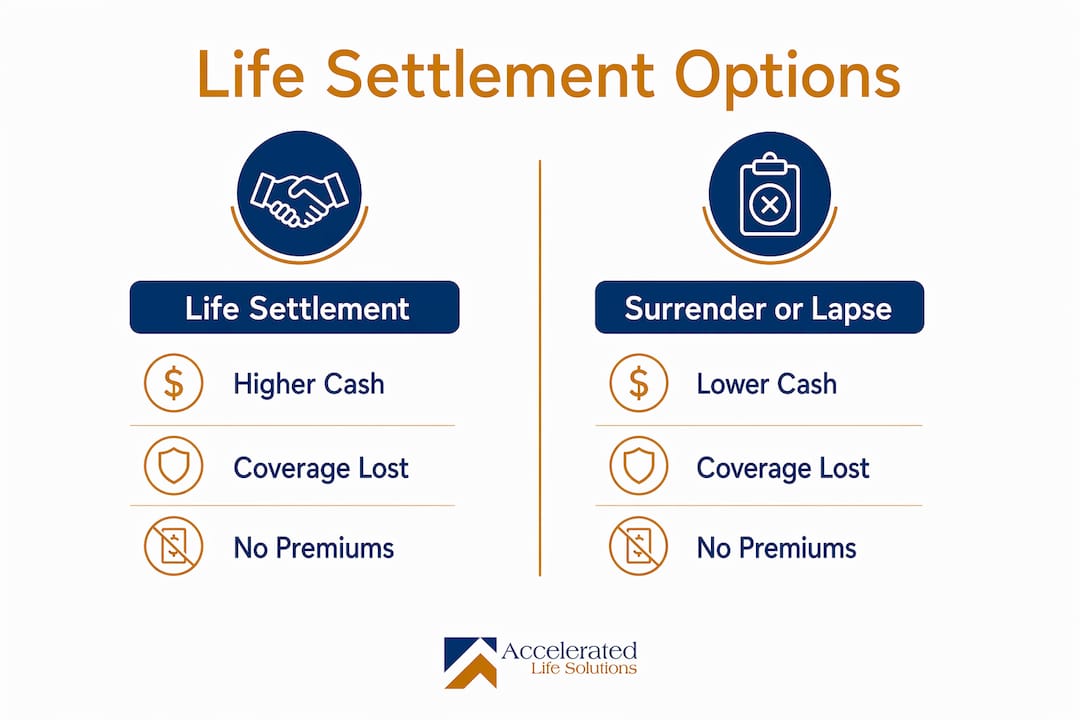

How do life settlements compare to surrendering or lapsing a policy?

The financial difference between a life settlement and the alternatives can be substantial. Settlement payouts frequently exceed cash surrender values by a significant margin. One documented example shows a surrender value of $74,000 against a life settlement offer of $612,000 after fees. That gap represents real money that seniors and their heirs forfeit when they lapse or surrender without exploring the secondary market.

| Option | Cash Received | Coverage Lost | Premium Obligation |

|---|---|---|---|

| Life settlement | More than cash surrender value, less than death benefit | Yes, transferred to buyer | Buyer assumes all future premiums |

| Policy surrender | Cash surrender value only | Yes, policy terminated | None after surrender |

| Policy lapse | Nothing | Yes, policy terminates | None, but all premiums paid are lost |

| Keep the policy | None | No | Ongoing, may create premium strain |

Surrendering a policy returns whatever cash value has accumulated, which is typically a fraction of the death benefit. Lapsing produces nothing at all. Both outcomes are permanent and irreversible. A life settlement, by comparison, monetizes the policy’s market value rather than just its internal accounting value.

The trade-off is real: selling the policy means the original beneficiaries will not receive the death benefit. Policyowners must weigh whether the immediate cash serves their current financial needs more effectively than a future inheritance would serve their heirs. For seniors managing retirement income, covering long-term care costs, or addressing estate liquidity needs, the calculus often favors the settlement. Reviewing a detailed lapse vs. life settlement comparison before making any decision is a practical first step.

How does a life settlement affect heirs and estate planning?

Once a life settlement closes, heirs no longer receive the policy death benefit. The transaction replaces a future inheritance with immediate cash in the hands of the seller. This shift in value is significant and requires deliberate planning, particularly when the policy was intended to fund a bequest, cover estate taxes, or support a surviving spouse.

A life settlement can serve as a deliberate estate liquidity strategy. The seller receives cash that can be redirected into other assets, gifted to heirs during their lifetime, or used to fund a smaller replacement policy if coverage is still needed. The key is that the decision is made consciously, not by default. Policyowners who allow a policy to lapse achieve the same result of no death benefit for heirs, but receive nothing in return.

Life settlements can also intersect with business succession planning. When a policy is held inside a buy-sell agreement, selling it through a life settlement rather than surrendering it can recover value that would otherwise be lost when the agreement is restructured or dissolved. Advisors reviewing how life settlement affects buy-sell agreements should factor this into any business transition analysis.

Pro Tip: If heirs are counting on a death benefit, discuss the settlement decision with them before proceeding. Transparency prevents disputes and allows the family to plan around the change in estate structure.

Regulatory safeguards protect sellers during this process. Most states codify a right to rescind the transaction within 15 days of receiving proceeds, giving sellers a cooling-off period to reconsider. This protection is especially relevant for older adults who may feel pressure to act quickly.

What regulations and broker compensation models govern life settlements?

Life settlements operate under a state-specific regulatory framework that provides meaningful protections for both buyers and sellers. The secondary market is well-regulated and transparent, with most states requiring broker licensing, disclosure of compensation, and adherence to anti-fraud provisions. The 2026 regulatory environment continues to emphasize consumer transparency and fiduciary accountability.

Key regulatory protections sellers should understand include:

-

Broker licensing: Life settlement brokers must hold a state-issued license in most jurisdictions. Unlicensed solicitation is a red flag.

-

Disclosure requirements: Brokers are required to disclose their compensation and any conflicts of interest before a transaction closes.

-

Right of rescission: Most states provide a 15-day window after receiving proceeds during which the seller can cancel the transaction without penalty.

-

Anti-fraud provisions: State insurance departments actively monitor the market for misrepresentation and predatory practices.

Licensed brokers are compensated through commissions drawn from the settlement proceeds, not from upfront fees charged to the seller. This structure means exploring the market carries no out-of-pocket cost to the policyowner. Life settlement broker fee structures vary, but commission percentages are disclosed in writing before any agreement is signed. Working with a fiduciary-minded broker who shops offers across multiple institutional buyers is the most reliable way to maximize proceeds and maintain compliance.

Comparing life settlement broker offers is not optional. A single offer from one buyer rarely represents the market’s best price. Brokers who access a broad pool of institutional buyers, including life settlement funds, hedge funds, and specialty investors, consistently produce higher offers than direct-to-provider transactions.

Key takeaways

A life settlement converts an underperforming life insurance policy into immediate cash, consistently paying more than surrender value and protecting seniors from the total loss of a lapse.

| Point | Details |

|---|---|

| Core definition | A life settlement sells a policy to a third party for more than surrender value but less than the death benefit. |

| Eligibility baseline | Policyowners aged 65 or older with permanent policies of at least $100,000 face value typically qualify. |

| Payout advantage | Documented cases show settlement offers exceeding surrender values by several times, making exploration worthwhile. |

| Heir impact | Selling transfers the death benefit to the buyer; heirs receive no future payout but benefit from the seller’s improved liquidity. |

| Broker compensation | Brokers are paid from proceeds, so sellers incur no upfront cost when exploring the market. |

Why life settlements deserve a place in every senior’s financial review

I have seen too many seniors surrender or lapse policies worth far more than their cash value, simply because no one raised the alternative. The assumption that life settlements are only for the very ill is one of the most persistent and costly misconceptions in personal finance. The decision to sell a policy should be based on whether it still serves the owner’s financial goals, not on a health threshold.

What surprises most people is how little downside there is to simply exploring the market. Getting a settlement offer costs nothing out of pocket. If the offer is not compelling, the policyowner keeps the policy. If it is, they have unlocked value that would otherwise disappear. That asymmetry makes exploration the rational default for any senior holding a policy they are considering surrendering or lapsing.

The heirs I have spoken with often express regret, not relief, when they learn a parent surrendered a policy months before passing. The cash surrender value was modest. The settlement value would have been substantial. That conversation is avoidable with proper planning and a trusted advisor who knows to ask the right questions. Real policyowner outcomes consistently reinforce this point.

My practical advice: before any senior or their advisor makes a final decision about a policy, request a life settlement evaluation. Treat it as a standard step in the review process, the same way you would compare annuity rates or review Social Security timing. The market has matured. The regulations are solid. The only remaining barrier is awareness.

— Brian Hurley

See what your policy is worth with Accelerated Life Solutions

Accelerated Life Solutions works exclusively as an independent life settlement broker, representing policyowners and their advisors, not institutional buyers. That independence means every offer is sourced competitively across the full market to maximize proceeds for the seller.

If you or a family member holds a life insurance policy that is no longer needed or has become a financial burden, the first step is understanding its market value. Use the life settlement calculator on the Accelerated Life Solutions website to get an initial estimate based on policy details and health status. For a personalized consultation and a full market evaluation, the broker services team at Accelerated Life Solutions is available to guide you through every step of the process with full transparency and regulatory compliance.

FAQ

What is a life settlement in simple terms?

A life settlement is the sale of a life insurance policy to a third-party buyer for a cash payment greater than the policy’s surrender value but less than its death benefit. The buyer takes over premium payments and collects the death benefit when the insured dies.

Who qualifies for a life settlement?

Most life settlement programs require the insured to be age 65 or older, hold a permanent life insurance policy with a face value of at least $100,000, and have maintained the policy in force for a qualifying period. Health status and life expectancy also influence eligibility and offer size.

How is a life settlement different from a viatical settlement?

A viatical settlement is designed for terminally ill policyholders with a limited life expectancy, while a life settlement serves seniors who are not facing an imminent health crisis but no longer need or can afford their coverage.

Can heirs still receive a death benefit after a life settlement?

No. Once the policy is sold, ownership transfers to the buyer, who becomes the sole beneficiary of the death benefit. The original heirs receive no future payout, but the seller receives immediate cash that can be redirected to support family members or estate goals.

Does exploring a life settlement cost anything upfront?

No. Life settlement brokers are compensated through commissions drawn from the settlement proceeds after a transaction closes. Policyowners pay nothing out of pocket to receive offers and evaluate the market.